Dollar Tree, Inc.

DLTR

posted mixed third-quarter fiscal 2021 results, wherein earnings beat the Zacks Consensus Estimate, while sales lagged the same. Meanwhile, sales improved year over year but earnings declined. Higher-than-expected freight costs in the reported quarter primarily hurt the bottom-line growth and gross margin. Compelling results from the H2, Dollar Tree Plus and the new Combo Stores, which are part of the company’s key initiatives, drove the third-quarter fiscal 2021 performance.

The company expects the elevated freight costs to remain headwinds in the near term. Consequently, the company narrowed its sales and earnings per share guidance range for fiscal 2022. This resulted in negative investor sentiments upon the company’s earnings release, leading to shares of Dollar Tree declining 1.9% in the pre-market session on Nov 23.

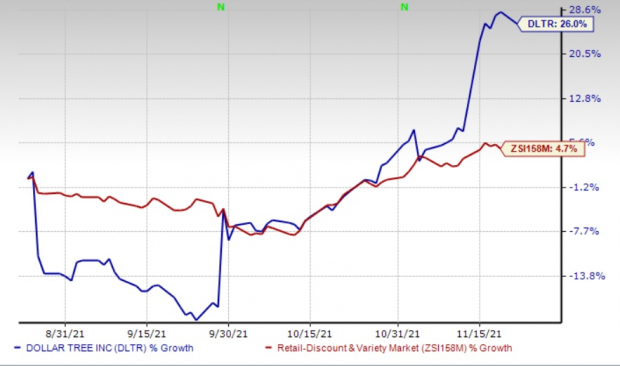

Shares of the Zacks Rank #3 (Hold) company have rallied 26% in the past three months compared with the

industry

‘s growth of 4.7%.

Image Source: Zacks Investment Research

Quarter in Detail

Dollar Tree’s earnings declined 30.9% year over year to 96 cents per share but surpassed the Zacks Consensus Estimate of 95 cents. The year-over year decrease can be attributed to the higher-than-anticipated freight costs witnessed in the quarter, which led to gross margin decline. However, earnings per share was better-than-expected owing to strong performance across its business. The company delivered earnings per share toward the high-end of the previously anticipated range of 88-98 cents per share.

Consolidated net sales rose 3.9% year over year to $6,417.7 million but fell short of the Zacks Consensus Estimate of $6,423 million. Enterprise same-store sales (comps) improved 1.6% year over year and 6.7% on a two-year basis. For the Dollar Tree banner, comps were up 0.6% on a constant-currency basis and 0.8% after adjusting for the impacts of Canadian currency fluctuations. Soft comps stemmed from weak performances at both Dollar Tree and Family Dollar segments. Comps for the Family Dollar banner rose 2.7%, compared with the robust 6.4% comps growth in the prior-year quarter.

Gross profit declined 8.3% year over year to $1,763.7 million, while gross margin contracted 370 bps to 27.5%. The decline in gross margin can be attributed to elevated freight costs, partly negated by continued improvement in shrink. Gross margin contracted 470 bps to 30.2% at the Dollar Tree banner and 240 bps to 24.4% at the Family Dollar segment.

Dollar Tree, Inc. Price, Consensus and EPS Surprise

Dollar Tree, Inc. price-consensus-eps-surprise-chart

|

Dollar Tree, Inc. Quote

Selling, general and administrative (SG&A) expenses, as a percentage of sales, declined 100 bps to 22.7%, driven by reduced COVID-related costs compared with the last year. In the year-ago quarter, the company incurred COVID-related costs of $35.3 million (or 57 bps).

While operating income declined 33.3% to $310.5 million, operating margin contracted 270 bps to 4.8% driven by soft gross margin partly offset by lower SG&A expense rate. Segment-wise, the operating margin contracted 420 bps to 8.5% for Dollar Tree and 160 bps to 3% at the Family Dollar segment.

Balance Sheet

Dollar Tree ended the quarter with cash and cash equivalents of $701.4 million. Net merchandise inventories increased 13.8% to $4,316 million. It had net long-term debt (excluding current maturities) of $3,231.1 million and shareholders’ equity of $7,244.4 million as of Oct 30, 2021. Outstanding debt as of the quarter-end was $3.25 billion.

In third-quarter fiscal 2021, the company did not repurchase any shares as it was focused on the launch of its broader nationwide $1.25 price point initiative. In the first nine months of fiscal 2021, the company bought back 9,156,898 shares for $950 million. As of Oct 30, 2021, the company had $2.5 billion remaining under its existing authorization.

For fiscal 2021, it expects to incur a capital expenditure of $1.1 billion. It anticipates utilizing the majority of the excess cash flow generated to repurchase shares under the aforementioned program.

Store Update

In third-quarter fiscal 2021, Dollar Tree opened 125 stores, expanded or relocated 34 outlets, and shuttered 23 stores. It completed the renovation of 450 Family Dollar stores to the H2 or Combo Store formats. As of Oct 30, 2021, the company operated 15,966 stores in 48 states and five Canada provinces.

Key Real Estate Initiatives Update

Dollar Tree is delivering compelling results for its key initiatives, which include the expanding footprint of the H2, Dollar Tree Plus and Combo Stores. The Family Dollar H2 stores have been performing well, with about 450 Family Dollar stores renovated to the H2 format in the fiscal third quarter. It currently has 3,300 Family Dollar H2 stores. In fiscal 2022, the company expects to complete 800 Family Dollar H2 Renovations as part of the Key Real Estate Initiative.

Its multi-price point Dollar Tree Plus concept store is gaining popularity among customers, particularly for discretionary categories. This has helped improve store productivity. Consequently, the company plans to accelerate the Dollar Tree Plus initiative by adding an additional 1,500 stores in fiscal 2022. It expects to have at least 5,000 Dollar Tree Plus stores by the end of 2024. It is on track to have 500 Dollar Tree Plus stores by the end of fiscal 2021.

The company’s newest format store — Combo Store — which leverages the strengths of both banners under one roof has exceeded expectations. Dollar Tree currently has 105 Combo Stores in operation. The company believes it has an opportunity for up to 3,000 Combo Stores in rural areas. Driven by the positive response, it expects the Combo Store to be the key strategic format, anticipating 85% of the newly opened Family Dollar stores to be Combo Stores in fiscal 2022. Thus, it expects 400 new or renovated Combo Stores for fiscal 2022.

Additionally, the company now plans to move away from its $1 pricing constraints and provide more value to customers through its $1.25 price point initiative. It plans to aggressively rollout the $1.25 price point to all Dollar Tree stores, with the new pricing introduced in more than 2,000 stores in December and all legacy Dollar Tree stores by the end of first-quarter fiscal 2022. The new pricing initiative is expected to enhance the company’s ability to expand its offerings, introduce new products and sizes, and provide families with more of their daily essentials. It will enable the company to reintroduce some of the customer favorites and traffic-driving products that were discontinued earlier due to the $1 pricing constraint.

Outlook

For fourth-quarter fiscal 2021, Dollar Tree expects consolidated net sales of $7.02-$7.18 billion, with comps growth in low-single digits. It anticipates earnings of $1.69-$1.79 per share.

For fiscal 2021, the company now expects net sales of $26.25-$26.41 billion compared with $26.19-$26.44 billion anticipated previously. It continues to expect comps growth in low-single-digits. Management now envisions earnings of $5.48-$5.58 per share, down from $5.40-$5.60 per share mentioned earlier. The narrowed earnings forecast was primarily due to the elevated costs that the company witnessed in the fiscal third quarter. The company expects to offset the higher freight costs through the gains from the transition of the Dollar Tree stores to the $1.25 price point. However, these gains will be partially negated by the one-time costs incurred for the transition of the stores.

Although transpacific ocean container rates have been in focus lately, Dollar Tree notes that it is being impacted by all aspects of freight, including higher costs for inland transportation by truck and rail. In the fiscal third quarter, the company moved more containers than anticipated, resulting in incurring higher-than-expected freight costs. The company expects the freight and supply chain disruptions to remain the greatest challenge in the near term.

The company’s Dollar Tree banner is extremely sensitive to higher freight costs due to its one-dollar price point. To overcome the situation, it is taking several steps to mitigate the impacts of higher freight costs and improve gross merchandise margin.

Better-Ranked Stocks in the Retail Space

We have highlighted three better-ranked stocks in the Retail – Wholesale sector, namely

Tractor Supply Company

TSCO

,

Costco Wholesale

COST

and

Target

TGT

.

Tractor Supply Company currently sports a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 22.8%, on average. Shares of TSCO have jumped 18.3% in the past three months. You can see

the complete list of today’s Zacks #1 Rank stocks here

.

The Zacks Consensus Estimate for Tractor Supply Company’s current financial year sales and earnings per share suggests growth of 19% and 23.9%, respectively, from the year-ago period’s reported figures. TSCO has an expected EPS growth rate of 9.6% for three-five years.

Costco currently carries a Zacks Rank #2 (Buy). The company has a trailing four-quarter earnings surprise of 7.7%, on average. Shares of COST have rallied 19.5% in the past three months.

The Zacks Consensus Estimate for Costco’s current financial year sales and earnings per share suggests growth of 9.6% and 9.7%, respectively, from the year-ago period. COST has an expected EPS growth rate of 8.6% for three-five years.

Target currently has a Zacks Rank #2. The company has a trailing four-quarter earnings surprise of 19.7%, on average. Shares of TGT have risen 8.5% in the past six months.

The Zacks Consensus Estimate for Target’s current financial year sales and earnings per share suggests growth of 14% and 39.6%, respectively, from the year-ago period. TGT has an expected EPS growth rate of 14.4% for three-five years.

Zacks’ Top Picks to Cash in on Artificial Intelligence

In 2021, this world-changing technology is projected to generate $327.5 billion in revenue. Now Shark Tank star and billionaire investor Mark Cuban says AI will create “the world’s first trillionaires.” Zacks’ urgent special report reveals 3 AI picks investors need to know about today.

See 3 Artificial Intelligence Stocks With Extreme Upside Potential>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report