Abiomed, Inc.

ABMD

is well-poised for growth in the coming quarters, backed by strength in its Impella product line. The optimism led by robust second-quarter fiscal 2023 performance along with positive tidings on the regulatory front are expected to contribute further. Headwinds from third-party reimbursement and forex woes persist.

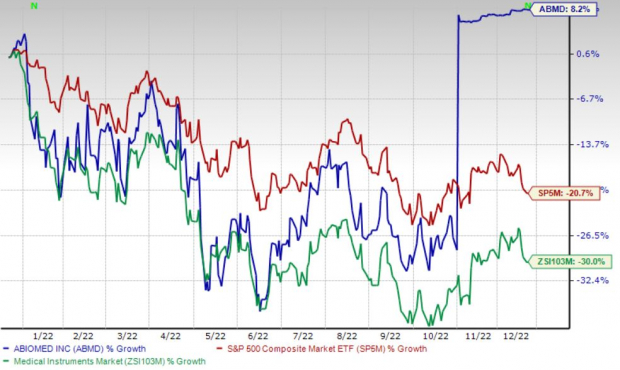

Over the past year, this Zacks Rank #3 (Hold) stock has gained 8.2% against 30% decline of the

industry

and 20.7% fall of the S&P 500 composite.

The renowned global provider of medical products designed to assist or replace the pumping function of the failing heart has a market capitalization of $17.18 billion. The company projects 25% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 15.6% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strength in Impella:

Abiomed’s flagship product line, Impella, has continued to be a growth driver, raising our optimism. The company is focused on achieving its Abiomed 2.0 goals, which will drive the rollout of its remote interface technology with SmartAssist and Impella Connect. Abiomed continues to invest in its pipeline of advanced technologies, including the XR Sheath, Impella ECP, Impella Connect, Impella BTR and new AI algorithms.

Regulatory Approvals:

Abiomed has been riding on a suite of regulatory approvals of late, which raises our optimism. This month, the company announced that the FDA had approved the version of Impella ECP that will be used in the Impella ECP Pivotal Trial, where the first two patients have been enrolled.

In October, Abiomed announced that Impella RP Flex with SmartAssist has received the FDA’s pre-market approval as safe and effective to treat acute right heart failure for up to 14 days.

Strong Q2 Results:

Abiomed’s solid second-quarter fiscal 2023 earnings buoy optimism. The company saw a year-over-year uptick in the top and bottom lines, and continued strength in its global Impella revenues. Abiomed’s robust geographical performance is also encouraging.

Downsides

Forex Woes:

Abiomed’s reported sales and earnings are subject to fluctuations in foreign currency exchange rates because some of its international sales are denominated in local currencies and not in U.S. dollars. The company, at present, does not hedge its exposure to foreign currency fluctuations from international operations. Therefore, revenues and expenses denominated in foreign currencies may be translated into U.S. dollars at less favorable rates, resulting in reduced revenues and earnings.

Third-Party Reimbursement:

Abiomed depends on third-party reimbursement to its customers for market acceptance of its products. Sales of medical devices largely depend on the reimbursement of patients’ medical expenses by government healthcare programs and private health insurers. Without government reimbursement or third-party insurers’ payments for patient care, the market for Abiomed’s products will be limited.

Estimate Trend

Abiomed is witnessing a negative estimate revision trend for fiscal 2023. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 3.9% south to $4.61.

The Zacks Consensus Estimate for the company’s third-quarter fiscal 2023 revenues is pegged at $293.2 million, suggesting a 12.3% improvement from the year-ago quarter’s reported number.

This compares to our third-quarter fiscal 2023 revenue estimate of $291.4 million, suggesting an 11.6% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are

Exact Sciences Corporation

EXAS

,

ShockWave Medical, Inc.

SWAV

and

Merit Medical Systems, Inc.

MMSI

.

Exact Sciences, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 27.5%. EXAS’ earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed the same in one, the average beat being 0.6%.

You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Exact Sciences has lost 32.9% compared with the

industry

’s 23.7% decline in the past year.

ShockWave Medical, carrying a Zacks Rank #2 at present, has an estimated growth rate of 22.2% for 2023. SWAV’s earnings surpassed estimates in all the trailing four quarters, the average beat being 146.1%.

ShockWave Medical has gained 20.6% against the industry’s 30% decline over the past year.

Merit Medical, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average beat being 25.4%.

Merit Medical has gained 10.6% against the

industry

’s 12.5% decline over the past year.

Zacks Top 10 Stocks for 2023

In addition to the investment ideas discussed above, would you like to know about our 10 top picks for the entirety of 2023? From inception in 2012 through November, the

Zacks Top 10 Stocks

portfolio has tripled the market, gaining an impressive +884.5% versus the S&P 500’s +287.4%.

Now our Director of Research is combing through 4,000 companies covered by the Zacks Rank to handpick the best 10 tickers to buy and hold. Don’t miss your chance to get in on these stocks when they’re released on January 3.

Be First to New Top 10 Stocks >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report