The Clorox Company

CLX

looks well-poised in a tough industry, driven by solid product demand and brand strength. The company is expected to continue gaining from its brand portfolio, innovation pipeline, cost-saving efforts and pricing actions. However, the impacts of the ongoing inflationary pressures and continued macroeconomic uncertainty might be deterrents for the company.

The Oakland, CA-based company’s top and bottom lines beat the Zacks Consensus Estimate in third-quarter fiscal 2022. The company’s sales rose 2% both year over year and on an organic basis. Sales gained from higher shipments across all segments, resulting in higher volume. Moreover, a flat price/mix and gains from its pricing actions boosted the top line.

Factors to Drive Growth

Clorox is on track with the IGNITE strategy, its latest and integrated strategy, formulated on a sturdy foundation of its 2020 Strategy. This initiative mainly focuses on the expansion of the key elements under the 2020 Strategy to pace up innovation in each area of business.

As a result, the company will be able to boost overall growth and reinforce competitive advantage, in turn, enhancing shareholder value. The IGNITE strategy mainly binds Clorox to four strategic areas — fuel growth through brand reinvestments, innovate to deliver enhanced customer experience, develop product portfolio and re-imagine the company’s operations.

IGNITE’s main principle is ‘Innovating for Good Growth,’ delivering sustainable and responsible growth. The IGNITE strategy encompasses the long-term financial targets of achieving net sales growth of 3-5%, EBIT margin expansion of 25-50 bps and a free cash flow generation of 11-13% of sales.

Clorox also remains on track with its cost-saving and productivity initiatives. Backed by the IGNITE strategy, the company aims for higher cost savings annually by emphasizing more on technology and integrated design. With this, it earlier expected to achieve an EBIT margin expansion of 175 bps annually. The company’s cost-based pricing strategy has enabled it to address the inflationary environment that has persisted for more than three years. These cost-saving and pricing actions should continue to support its investment in long-term brands and category growth.

Management has announced plans to invest $500 million in the next five years, beginning fiscal 2022. Of this, the company plans to invest $90 million in fiscal 2022 for digital capabilities and productivity enhancements. As part of the investment, it will replace the enterprise source planning system, which will help generate efficiencies and position it better in supply chains, digital commerce, innovation and brand building for the long term.

The company is witnessing strong progress in the core International business as it continues to build on the success of the segment’s Go Lean strategy. These efforts will help accelerate growth for the segment. Driven by its IGNITE Strategy, which aims to improve profitability in International business, the company expects to invest selectively in profitable platforms. Management continues to explore international opportunities, including the acquisition of a majority stake in its joint venture in the Kingdom of Saudi Arabia. The company believes that the acquisition can boost long-term growth in the international segment.

In third-quarter fiscal 2022, sales at the International segment rose 1% year over year on a favorable price mix, and increased shipment volume, primarily for cleaning and disinfecting, and cat litter products. Organic sales for the segment improved 6%.

Headwinds to Overcome

Elevated manufacturing and logistics costs, and higher commodity costs have been hurting the company’s gross margin despite the gains from pricing actions and cost-saving initiatives. The gross margin contracted 760 basis points (bps) to 35.9% in the fiscal third quarter. Also, long-term brand investments to support its innovation pipeline and customer engagement efforts have been resulting in higher selling and administrative expenses for the past few quarters. It has also been incurring incremental spending on advertising and sales promotion to support sales growth.

Clorox expects the operating costs to remain high in fiscal 2022. The company projects selling and administrative expenses, as a percentage of sales, of 14-15% for fiscal 2022. The view includes 1% of this impact from the planned investments in digital capabilities and productivity enhancements.

Clorox expects to invest $90 million in long-term strategic digital capabilities and productivity enhancements in fiscal 2022. Of this, it expects $73 million (45 cents per share) to flow through to the profit and loss statement, most of which is expected to be recorded in selling and administrative expenses. It expects advertising and sales promotion expenses to be 10% of net sales.

Bleak View

Clorox updated its fiscal 2022 view to take into account the adverse impacts of cost inflation and the volatile operating environment. The company’s guidance also includes the uncertainty regarding the war in Ukraine.

The gross margin for fiscal 2022 is expected to decline 800 bps, owing to higher-than-anticipated commodity costs, and manufacturing and logistics expenses. Consequently, adjusted earnings for fiscal 2022 are estimated to be $4.05-$4.30 per share, suggesting a year-over-year decline of 44-41%. The company notes that adjusted earnings per share will exclude long-term investments in digital capabilities and productivity enhancements to provide greater visibility to the underlying operating performance.

On a GAAP basis, earnings per share are anticipated to be $3.60-$3.85, suggesting a decline of 35-31% from the year-ago period. The company envisions a sales decline of 1-4%, both on a reported and organic basis, for fiscal 2022. For the first half of fiscal 2022, sales are likely to decline 7%. The effective tax rate is anticipated to be 22-23%.

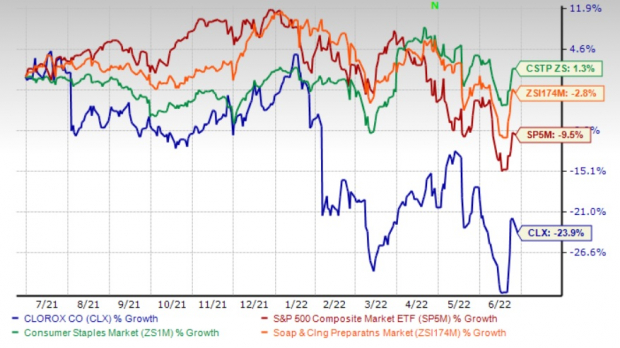

Shares of this Zacks Rank #3 (Hold) company have declined 23.9% in the past year compared with the

industry

‘s decline of 2.8%. The stock also underperformed the sector’s gain of 1.3% and the S&P 500’s decline of 9.5% in the past year.

Image Source: Zacks Investment Research

Stocks to Consider

We have highlighted three better-ranked stocks in the Consumer Staples sector, namely

Archer Daniels Midland

ADM

,

Fomento Economico Mexicano

FMX

and

The Coca-Cola Company

KO

.

Archer Daniels, the Delaware, IL-based leading producer of food and beverage ingredients and goods made from various agricultural products, presently sports a Zacks Rank #1 (Strong Buy). The ADM stock has rallied 25.4% in the past year. You can see

the complete list of today’s Zacks #1 Rank stocks here

.

The Zacks Consensus Estimate for Archer Daniels’ sales and EPS for the current financial year suggests growth of 12.3% and 22%, respectively, from the year-ago reported levels. The consensus mark for earnings has moved up 3.3% in the past 30 days. ADM has a trailing four-quarter earnings surprise of 22.3%, on average. It has an expected long-term earnings growth rate of 6.4%.

Fomento Economico Mexicano, alias FEMSA, has exposure in various industries, including beverage, beer and retail, which gives it an edge over its competitors. It presently has a Zacks Rank of 2 (Buy). FEMSA has a trailing four-quarter earnings surprise of 3.9%, on average. Shares of FMX have declined 20.2% in the past year.

The Zacks Consensus Estimate for FEMSA’s sales for the current financial year suggests growth of 5.3% from the year-ago period’s reported figure. The same for earnings per share suggests a fall of 7.1%. The current financial year’s earnings per share have moved down 1.6% in the past 30 days. FMX has an expected EPS growth rate of 8.8% for three to five years.

Coca-Cola currently has a Zacks Rank #2. The company has an expected long-term earnings growth rate of 7%. Shares of KO have risen 15.1% in the past year.

The Zacks Consensus Estimate for Coca-Cola’s current financial year’s earnings per share has been unchanged in the past 30 days. The Zacks Consensus Estimate for KO’s sales and EPS for the current financial year suggests growth of 8.9% and 6.5%, respectively, from the year-ago reported levels. KO has a trailing four-quarter earnings surprise of 13.6%, on average.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report