Companies in the Semiconductor – General industry are at the forefront of the ongoing technological revolution based on HPC, AI, automated driving, IoT and so forth. These semiconductors also enable the cloud to function and help analyze the data into actionable insights that can be used by companies to operate more efficiently.

The pandemic led companies to ramp up technology investments in order to stay operational when it was unsafe for us to go to work or meet people. But this brought forward several years of investments, weakening the near-term outlook. With the financial tightening increasing the possibility of a recession in 2023, it has become notable harder to predict the impact on this industry.

Additionally, supply chains are adjusting to increase reliability, build some inventory, reduce dependence on China, and onshore projects with national security implications. All these factors are contributing to increased uncertainty and as a result, the valuation is also looking rich. Longer-term trends continue to favor strong growth due to auto electrification, structural changes in industrial automation, data center strength, and increased adoption of the cloud, AI, IoT, etc.

Despite these concerns, STMicroelectronics and Sumco Corp. may be worth considering.

About the Industry

The companies grouped under the Semiconductor – General category produce a broad range of semiconductor devices, both integrated and discrete, like microprocessors, graphics processors, embedded processors, chipsets, motherboards, wireless and wired connectivity products, DLPs and analog, serving multiple end markets. It includes companies like NVIDIA, Texas Instruments, Intel and STMicroelectronics.

According to the latest data from the Semiconductor Industry Association (SIA), global semiconductor sales growth in the third quarter of 2022 declined 3% from the prior year, reaching $141 billion. Gartner forecasts semiconductor revenue to grow about 4% this year before declining 3.6% in the next. While macro concerns are impacting near-term performance, the long-term outlook is solid.

Major Themes Shaping the Industry

-

The long-term outlook for the industry remains robust because of its being on the building-block side of technology, which makes it crucial for the proliferation of the Internet and the ongoing digitization of every aspect of life. The

short-term outlook

appears bleak however. The pandemic has accelerated the move toward digitization, but it has created a lot of imbalances in demand and supply. The smartphone market for example (a primary application of semiconductors) is seeing issues on both the demand and the supply sides. Demand is affected by inflation while supply is affected by not only inflation but also geo-political tensions, China shutdowns and ongoing supply chain constraints. The other major chip consumer is the PC market, where the consumer and education segments remain soft following two years of very strong growth. With global economies engaged in financial tightening, there is the concern that demand could weaken significantly over the next year or so.

-

The good news is that some of the weakness in these traditional markets is being made good by

strength in emerging areas

like AI and machine learning, IoT, and automotive. ReportLinker expects the AI chip market to grow at a CAGR of 29.9% between 2022 and 2030. Driven by Internet connectivity across the developed and developing worlds and supportive technology such as sensor networks and AI adoption, the IoT market is also expected to grow steadily over the next few years. Future Market Insights expects the market to grow at a 5.3% CAGR between 2022 and 2032. Mordor Intelligence expects a stronger 14.7% CAGR between 2022 and 2027. Automotive electronics is another area of evolving needs with increasing electronics (including ADAS), safety enhancements and transition to electrified power trains being important drivers. Grand View Research estimates a 10.7% CAGR through 2025, which it attributes to awareness regarding energy-efficient lighting systems, as well as increasing sales of luxury vehicles that come fitted with navigation and infotainment systems. Automation and robotics, with increasing adoption across industrial operations, are other areas of growth. These strong end markets will drive continued demand for semiconductor components for years to come.

-

Semiconductor supply chains are adjusting

. Semiconductor supply chains have become increasingly efficient over the years. While this has brought down cost, the just-in-time model has made the supply chains relatively unreliable in case of external disruptions, as happened during the pandemic, or when China imposed its zero tolerance COVID shutdowns. This, along with the recently-imposed restraints on dealing with China has led semiconductor companies to diversify their supply chains and reduce their dependence on China. This is an ongoing process that will take several years. In the meantime, there is a growing concern that all the most important leading-edge chips are currently made in Taiwan, a country that China threatens to annex all the time. Since this has national security implications, there is an ongoing drive to onshore manufacturing. The $52 billion infusion from the CHIPS Act will help.

Zacks Industry Rank Indicates Uncertain Prospects

The Zacks

Semiconductor-General

industry is a stock group within the broader Zacks

Computer and Technology

sector. It carries a Zacks Industry Rank #90, which places it in the top 36% of the nearly 250 Zacks-classified industries.

The group’s Zacks

Industry Rank

, which is basically the average of the Zacks Rank of all the member stocks, indicates that near-term prospects aren’t too bright. Our research shows that the bottom 50% of the Zacks-ranked industries underperforms the top 50% by a factor of 1:2.

An industry’s positioning in the top 50% of Zacks-ranked industries is normally because the earnings outlook for the constituent companies in aggregate is relatively strong. The opposite is true for stocks in the bottom 50% of industries. In this case, the aggregate earnings estimate for 2022 is down 27.8% from the year-ago level. The aggregate earnings estimate for 2023 is down 32.2% from last year. The numbers have deteriorated significantly since July.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

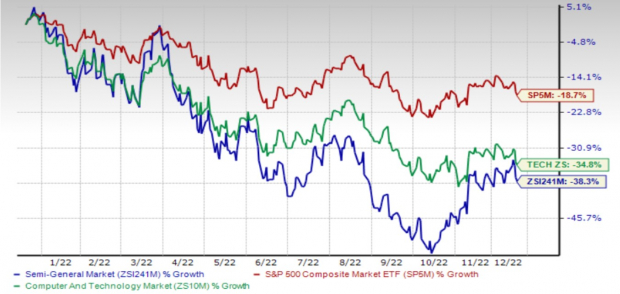

Industry Lags on Stock Market Performance

Tracking the performance of the Zacks Semiconductor – General Industry over the past year shows that the industry has traded below than both the broader Zacks Computer and Technology Sector and the S&P 500 index since April of this year. As of now, it trails both the industry and the S&P 500.

The industry lost 36.0% of its value over the past year compared to the 33.1% loss of the broader sector and the 17.2% loss of the S&P 500 index.

One-Year Price Performance

Image Source: Zacks Investment Research

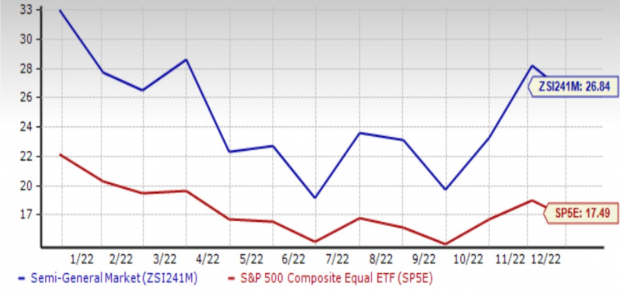

Industry’s Current Valuation

On the basis of forward 12-month price-to-earnings (P/E) ratio, which is a commonly used multiple for valuing semiconductor companies, we see that the industry is currently trading at 27.24X, which is above its median level of 23.47X over the past year. However, the S&P 500 trades at 17.15X while the sector trades at 20.23X. Therefore, the industry appears overvalued in all respects.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

2 Stocks Worth Considering

STMicroelectronics N.V. (

STM

)

: The company designs, develops, manufactures and markets a broad range of semiconductor integrated circuits and discrete devices used in a wide variety of microelectronic applications, including telecommunications systems, computer systems, consumer products, automotive products and industrial automation and control systems.

STMicroelectronics is seeing strong demand across all segments with particular strength in the automotive and B2B industrial markets. Backlog is solid and covers six to eight quarters of planned capacity and the book-to-bill remains above 1. Therefore, demand is extremely strong and utilization is 100%.

The strength in auto is coming from the ongoing electrification and digitalization, increased semiconductor content in legacy auto and replenishment across the automotive supply chain. Demand is currently stronger than available and planned capacity through 2023.

Factory automation and infrastructure investment will continue in the industrial market, which is the other significant end market for STMicroelectronics. The increase in semiconductor content, digitalization of devices and systems, energy management and power efficiency improvements, and building and home control are the biggest drivers.

The pricing strength that STM is seeing this year may not continue next year but mix is expected to remain a positive contributor to margins.

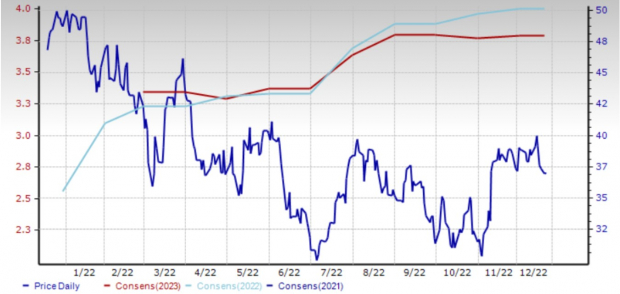

STM beat the Zacks Consensus Estimate by 11.5% in the last quarter. In the last 60 days, the current year EPS estimate of this Zacks Rank #2 (Buy) stock increased 13 cents (3.4%).

The shares of the company are down 21.6% over the past year, despite the spike after very strong third-quarter results.

Price & Consensus: STM

Image Source: Zacks Investment Research

Sumco Corp.

SUOPY

: Tokyo-based Sumco manufactures and sells silicon wafers for the semiconductor industry primarily in Japan, the U.S., China, Taiwan and Korea.

Consistent with industrywide trends, #3 (Hold) ranked Sumco is seeing strength in automotive, industrial and data center markets and softness in PC and consumer markets. As a result, management has said that 300mm and 200mm production will continue as planned while production for 150mm wafers will continue to be moderated in line with consumer market demand.

At any rate, demand for state-of-the-art wafers is expected to remain strong. Therefore, capital investment will also continue as planned last year in new plant buildings, and in utility and manufacturing equipment. Additionally, AI-enabled productivity improvements will continue. Geopolitical conditions, US-China tensions and financial tightening in economies across the world have not had a material impact on results so far. But that situation can change quickly since semiconductor supply chains are still very efficient with relatively short lead times.

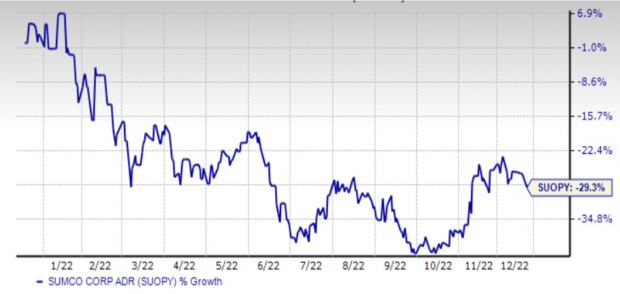

There is no change in the Zacks Consensus Estimate for 2022 and 2023 in the last 90 days.

The Zacks Rank #3 stock is down 11.4% in the past year.

Price: SUOPY

Image Source: Zacks Investment Research

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report