As we get into the final days of the year, it’s a good time to plan for next year.

This hasn’t been the best of years for the stock market, mainly because of earlier actions to boost the economy with quantitative easing. But inflation went up to 40-year highs and the Fed finally changed course in the first quarter of this year. Through 7 meetings, the federal funds rate was raised by a total of 4.25%. This increased borrowing costs for individuals and businesses, slowing down the economy and leading to some moderation in prices.

Historically, the Fed has never managed to do this without the economy falling into recession. So experts are divided on whether we will actually have a recession next year. There’s one camp that says that things will turn worse in the first half itself. There’s another camp that says it will take longer, perhaps moving into 2024, mainly because the labor market is just too strong at the moment.

The Fed would like its actions to also raise the unemployment levels because until that happens, there won’t be sufficient cause to bring prices back to normal. However, there are labor shortages in most industries and a certain reluctance to let skilled or experienced people go. Technology is an exception, since it bulked up during the pandemic and is now offloading. As long as people are employed, they will continue to try and absorb higher prices, so inflation will be hard to bring down.

With that as the backdrop and further rate hikes lined up for 2023, the following year is also likely to be challenging. One way to deal with this is to aim for value stocks. As the markets have softened notably this year, valuations have come down, making this a great time to shop value.

Another strategy would be to select stocks that analysts expect have both near-term and longer-term growth potential. Even before getting into the details of each stock, we can skim through the numbers for a general idea.

In the examples discussed below, some of these numbers have been highlighted. The Zacks Rank, industry position, the estimate revisions history, surprise history, near-term and longer-term growth potential and analyst expectations of a rally next year, in combination, give you a pretty good idea. After shortlisting in this way, you can get into further details on each stock.

Altair Engineering Inc.

ALTR

Zacks Rank #2

: The Zacks Rank is sensitive to changes in estimates. Therefore, Zacks #1 (Strong Buy) ranked stocks reflect positive estimate revisions in the recent past while #2 (Buy) ranked stocks reflect positive estimate revisions from a little further back (or it can represent slight moderation in estimates also).

In the case of Altair, the Zacks Consensus Estimate for 2023 has dropped a penny in the last 60 days. It may be harder to develop estimates for smaller companies since they usually grow at a faster rate. Analysts have been duly conservative as regards Altair, as reflected in the average surprise of 145.6% in the last four quarters.

Zacks Industry Rank 61/248 (top 25%)

: The Engineering – R and D Services industry to which Altair belongs has returned over 8% to investors this year, which compares favorably with the S&P 500’s nearly 21% loss. Its revenues plunged significantly in 2020 as the pandemic ravaged the world and have been increasing very gradually since then.

Earnings have, however, recovered to pre-pandemic levels. Therefore, the ability to quickly take down cost when necessary, seems to be a basic characteristic. The leaner operating structure should stand it well in case of softer demand in 2023. On the other hand, relatively stronger demand could raise profitability.

Also encouraging is the fact that 80% (12) of the 15 companies that have reported results for this quarter have topped analyst estimates, 13% (2) met estimates while 7% (1) missed.

A buy-ranked stock in the top 50% of Zacks-classified industries has historically been seen to outperform stocks in the bottom 50%. Therefore, this is an indication of relative strength for Altair by virtue of its belonging to an attractive industry.

Strong Growth Profile

: Current estimates for 2023 represent a 21.5% increase in earnings and 8.0% increase in revenue over 2022 levels. Therefore, recession or not, analysts are extremely optimistic about the stock’s growth next year. They’re also positive about its long-term prospects, as indicated in the 12% growth forecast for the long term.

Upside Potential

: The average target price fixed by analysts represents 30.4% upside from the current level of $44.59.

ChampionX Corp.

CHX

Zacks Rank #2

: The Zacks Rank reflects positive estimate changes for 2023. The Zacks Consensus Estimate for the year is up 22 cents (13.9%). There is a reasonable possibility that the company will beat the raised number since it has topped estimates in each of the last four quarters at an average rate of 9.6%.

Zacks Industry Rank 61/248 (top 25%)

: Like Altair, ChampionX belongs to the Engineering – R and D Services industry, so the same positives apply to it as well.

Strong Growth Profile

: Current estimates for 2023 represent an 8.0% revenue increase and 46.3% earnings increase over 2022 levels. Therefore, analysts are pretty optimistic about growth next year. They’re also positive about its long-term prospects, as earnings are expected to grow 57.8% in the long term.

Upside Potential

: The average target price fixed by analysts represents 17.6% upside from the current price of $28.59.

ASML Holding N.V.

ASML

Zacks Rank #2

: This Zacks Rank indicates that analysts have been raising their estimates on ASML shares and we can see the evidence in the numbers. In the last 60 days, the 2023 estimate has increased 70 cents (3.5%).

ASML is a well-established semiconductor equipment supplier. It supplies leading edge technology for a market that is rapidly expanding. Therefore, there is underlying strength in the business that is likely to override any near-term weakness we may see as a result of the Fed’s money market manipulations. This is probably why analysts haven’t been as good at figuring out its growth potential. Therefore, we see that the average earnings surprise for the last four quarters is as high as 37.9%.

Zacks Industry Rank 47/248 (top 19%)

: Clearly, the Semiconductor Equipment – Wafer Fabrication industry is attractive and offers strong growth potential for its constituents. All of the companies that have reported results thus far have topped estimates.

Being a high-growth segment, it has been beaten down 33.4% so far this year. But unlike other growth segments, this one has not faltered materially after the strong tech buildup during the worst of the pandemic. Here, we see more or less steady revenue and earnings growth to way above pre-pandemic levels.

Strong Growth Profile

: In 2023, analysts expect revenue to grow 23.0% and earnings to grow 41.2%. They are projecting 23.7% growth for the long term.

Upside Potential

: The average target price that analysts have set represents 30.0% appreciation from the current price of $551.37.

Datadog, Inc.

DDOG

Zacks Rank #2

: The Buy rating on Datadog shares indicates that estimate revisions have been positive. And so we see that the Zacks Consensus Estimate for 2023 has moved up 14 cents (14.7%).

The company has been growing its earnings at such a rapid pace that analyst estimates have been left in the dust. The surprise percentage in the last four quarters averages 81.2%.

Zacks Industry Rank 54/248 (top 23%)

: The rank indicates that the Internet – Software industry to which Datadog belongs is attractive. Out of the total 139 companies within this industry, 101 (73%) have topped the Zacks Consensus Estimate in the latest quarter. About 8% met estimates while 15% missed.

It’s worth noting that the constituent companies may actually be very different from each other and cater to different use cases/industries. So numbers for the total industry may not reflect the good news in several of the segments.

Strong Growth Profile

: Datadog is currently expected to grow its 2023 earnings by 20.1% on top of revenue that is expected to grow 33.7%. Strong earnings growth is expected to continue over the next few years, averaging to a long-term rate of 42.9%.

Upside Potential

: The average target price indicates that analysts expect Datadog shares to appreciate 57.2% from the current price of $72.42.

Tenaris S.A.

TS

Zacks Rank #2

: It’s the estimates that drive changes in the Zacks Rank. And estimates for Tenaris have been moving up. The Zacks Consensus Estimate for 2023 has gone up 60 cents in as many days to $5.18. This is a 13% increase in a relatively short timeframe, indicating increased optimism.

Although the company missed by a penny in the last quarter, the average surprise in the last four quarters is 20.9%. Therefore, there’s reason to believe that another beat is around the corner.

Zacks Industry Rank 18/248 (top 7%)

: The Steel – Pipe and Tube industry to which Tenaris belongs has things going for it. Barring the June 2022 quarter, revenue and earnings have been moving up pretty consistently since the pandemic hit in the June quarter of 2020. As a result, it has returned 45.4% to investors this year.

Two out of the four companies in this industry that have reported earnings this quarter have topped estimates.

The 2023 estimate for this industry has moved up 70.4% so far this year.

Strong Growth Profile

: Tenaris is currently expected to generate 21.1% revenue growth and 19.6% earnings growth in 2023. Analysts expect earnings growth of 27.0% in the long term.

Upside Potential

: The average target price indicates an upside potential of 25.0%.

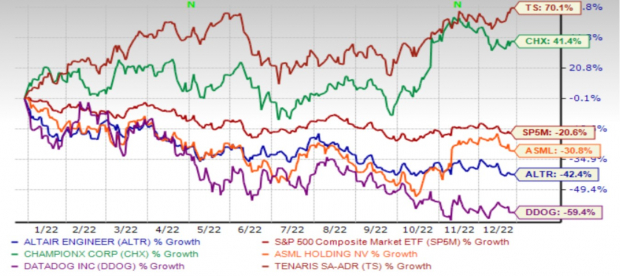

Price Performance Year-to-Date

Image Source: Zacks Investment Research

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.8% per year. So be sure to give these hand-picked 7 your immediate attention.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report