TopBuild Corp.

BLD

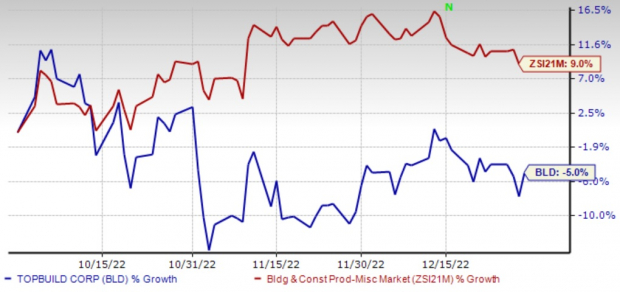

shares have dropped 5% in the past three months versus the Zacks

Building Products – Miscellaneous

industry’s 9% growth. The company has been grappling with supply-chain disruptions, higher raw material and labor shortages, and seasonality.

Analysts are pessimistic about BLD’s near-term prospects, as evident from the recent estimate revision trend. Earnings estimates for 2023 have fallen in the past 30 days from $15.30 to $14.58 per share. For 2023, earnings estimates reflect a 12.9% decline on a 6.7% revenue decrease.

Nonetheless, this installer and distributor of insulation and other building products has a unique business model combining both installation and specialty distribution, operating efficiency along with strategic buyouts.

Image Source: Zacks Investment Research

Let’s check the factors substantiating this Zacks Rank #3 (Hold) company. You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

.

Growth Driving Factors

Solid Operational Model

: The company has solid business operational models, comprising Installation and Specialty Distribution segments. The Installation segment primarily installs insulation and other building products, while the Specialty Distribution segment mainly sells and distributes insulation and other building products. Given the solid model, the company has been recording solid earnings and revenue growth over the last few quarters.

During the first nine months of 2022, the company’s sales increased 54.5%, adjusted earnings per share grew 64.4%, adjusted gross margin expanded 110 bps and adjusted EBITDA margin expanded 130 bps from the prior-year period. The impressive margin expansion led to increased profitability, depicting a flexible operating model and its ability to quickly reduce costs.

Upbeat View

: TopBuild lifted its 2022 views and expects a strong fourth quarter performance. It now expects sales between $4.95 billion and $5 billion for 2022 versus $4.80-$4.90 billion expected earlier. The estimated figure indicates an increase from $3.49 billion reported a year ago. Adjusted EBITDA is now projected within $915-$935 million compared with $860-$900 million projected earlier. This suggests growth from $605.9 million reported in 2021. For the remainder of 2022, although the residential market has slowed, the company expects demand to remain solid across the other two end markets it serves: commercial and industrial.

Inorganic Strategy

: BLD’s systematic inorganic strategy has been supplementing organic growth and expanding access to additional markets and products. During the first nine months of 2022, BLD made five acquisitions, which are expected to contribute $17.3 million in annual revenues. On Jul 21, 2022, the company acquired CV Insulation, LLC.

The company has a strong pipeline of prospective acquisitions, mainly focused on the insulation business, which accounted for 79% of the Installation segment’s sales in 2021.

Headwinds

Inflation Ails

: Unprecedented supply-chain disruptions and higher raw material and labor costs remain concerns for TopBuild. Labor shortages and material constraints are stretching the building cycle and increasing the lag time. The cost of fiberglass has increased frequently in recent times. In fact, the four fiberglass manufacturers have announced a 10% increase in prices, effective from December or early January 2022. This apart, supply chain disruptions are bothering the whole industry, including TopBuild.

Seasonal Woes

: TopBuild’s business has historically been subjected to seasonal influences. The company typically realizes higher sales in the third and fourth calendar quarters, which correspond with the peak season for residential new construction and residential repair/remodel activity. Winter sales are seasonally slower due to lower construction activity. Hurricanes, severe storms, earthquakes, droughts, floods, fires and other natural disasters also hamper its performance.

Key Picks

Some better-ranked stocks that warrant a look in the Zacks

Construction

sector include

EMCOR Group Inc.

EME

,

Altair Engineering Inc.

ALTR

and

ChampionX Corp.

CHX

, each carrying a Zacks Rank #2 (Buy).

EMCOR

: Headquartered in Norwalk, CT, this heavy construction company provides electrical and mechanical construction and facilities services in the United States. EMCOR has been benefiting from solid execution in the U.S. Construction segment — comprising the U.S. Mechanical and Electrical Construction units — as well as disciplined cost control. Also, accretive buyouts have been strengthening its overall results by adding new markets, opportunities and capabilities.

EMCOR’s 2023 earnings estimates have increased to $9.10 per share from $8.79 over the past 60 days. Earnings for 2023 are expected to grow nearly 17%.

Altair

: This Troy, Michigan-based company provides software and cloud solutions in simulation, high-performance computing, data analytics and artificial intelligence worldwide. Despite significant macroeconomic uncertainty, ALTR has been registering solid growth in billings on a constant-currency basis and witnessing strong demand across all geographies. The company’s focus on delivering services with outstanding technology developments and applications is expected to drive growth.

Altair’s earnings for 2023 are expected to witness 21.5% growth from the year-ago report.

ChampionX

: This engineering services company provides chemistry solutions, engineered equipment and technologies to companies that drill for and produce oil and gas. CHX’s Chemical Technologies offering consists of chemistry solutions for flowing oil and gas wells as well as chemistry solutions used in drilling and completion activities. The company has successfully implemented price increases and surcharges to offset cost inflation. Moreover, CHK remains optimistic about the constructive demand tailwinds in its businesses that support a favorable multi-year outlook for the sector.

ChampionX has an expected earnings growth rate of 46.3% for the next year. The Zacks Consensus Estimate for next-year earnings has improved 4.7% over the last 30 days.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report