Dillard’s Inc.

DDS

has been favored by investors for quite some time, owing to its robust quarterly results on improved margins and lower expenses. Notably, the company’s aggressive measures to lower excess inventory, owing to the pandemic-led decline in demand, have been aiding the gross margin.

Also, the ongoing vaccination drive and government stimulus packages have aided the recovery in consumer demand and store traffic trends. These factors led to the better-than-expected top and bottom-line results for first-quarter fiscal 2021.

The company retained investors’ bullish sentiments by maintaining its earnings beat streak in all of the last four quarters, the average being 206.3%. Also, the top line surpassed estimates in the last four quarters. This, in turn, underlines its operational excellence.

In the past 30 days, the company’s estimates for fiscal 2021 and 2022 earnings per share have moved up 542.3% and 127%, respectively. For fiscal 2021, its earnings estimates are pegged at $14.26 per share, suggesting significant growth from a loss of $2.73 reported in the prior-year quarter.

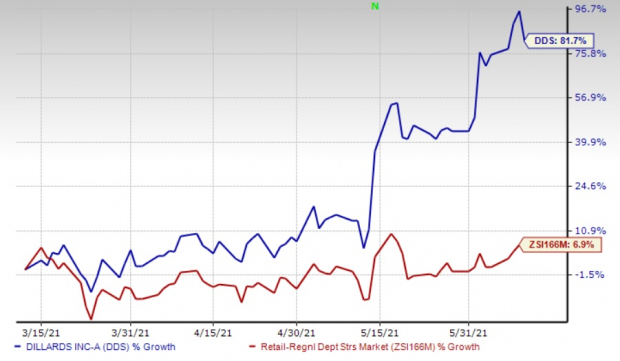

Moreover, the Zacks Rank #1 (Strong Buy) stock has gained 81.7% in the past three months compared with the

industry

’s growth of 6.9%. Also, the company’s shares have rallied 59.5% since reporting robust first-quarter fiscal 2021 results on May 12, 2021.

Image Source: Zacks Investment Research

Now let us discuss at length what makes the large departmental store chain an investor favorite.

Dillard’s has been keen on inventory management since the start of the pandemic through measures like cancellation, suspension and delaying of shipments as well as merchandise purchase reduction. The aggressive measures to lower excess inventory, owing to the pandemic-led decline in demand, have proved beneficial for the company’s margins.

As of the end of first-quarter fiscal 2021, inventory declined about 17% year over year to $1,306.5 million. Prior to this, inventory levels were down 26%, 22%, 20% and 14% in the fourth, third, second and first quarters of fiscal 2020, respectively.

Moreover, inventory reductions resulted in lower markdowns in the fiscal first quarter, which boosted the gross margin. Notably, the retail gross margin improved significantly to 42.7% from 12.8% in the year-ago quarter. On a consolidated basis, the gross margin of 41.7% reflects a sharp improvement from 12.5% in the prior-year quarter.

Also, Dillard’s has taken several steps to reduce costs, starting from first-quarter fiscal 2020, which have been retained in the first quarter of fiscal 2021. Some of these are the extension of vendor payment terms, the reduction of discretionary and capital expenditure, and payroll deduction. Backed by the efforts, the company’s retail SG&A expenses (operating expense) declined 17% year over year to $335.1 million in the fiscal first quarter. Dillard’s consolidated SG&A expenses (as a percentage of sales) contracted significantly to 25.3% from the prior-year quarter’s 36.9%, owing to lower payroll and a decline in payroll expenses.

These positive along with the acceleration of the vaccination program, an increase in stimulus money and favorable weather boosted the top and bottom lines in the reported quarter. Net sales surged 69% year over year, with total retail sales rising 73% year over year. Solid performance in juniors and children’s apparel, men’s apparel and accessories, and ladies’ accessories and lingerie contributed to sales growth.

Conclusion

Backed by the progress on its robust inventory and cost-management efforts, we expect the company to retain its business momentum in the near term.

Other Retail Stocks to Watch

Abercrombie & Fitch Company

ANF

has a long-term earnings growth rate of 18%. It currently sports a Zacks Rank #1. You can see

the complete list of today’s Zacks #1 Rank stocks here

.

The Children’s Place, Inc.

PLCE

, also a Zacks Rank #1 stock, has an expected long-term earnings growth rate of 8%.

Kohl’s Corporation

KSS

has a long-term earnings growth rate of 8%. It currently has a Zacks Rank #2 (Buy).

+1,500% Growth: One of 2021’s Most Exciting Investment Opportunities

In addition to the stocks you read about above, would you like to see Zacks’ top picks to capitalize on the Internet of Things (IoT)? It is one of the fastest-growing technologies in history, with an estimated 77 billion devices to be connected by 2025. That works out to 127 new devices per second.

Zacks has released a special report to help you capitalize on the Internet of Things’s exponential growth. It reveals 4 under-the-radar stocks that could be some of the most profitable holdings in your portfolio in 2021 and beyond.

Click here to download this report FREE >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report