The Zacks Rank is one of the best stock rating systems out there, but at any given time there are hundreds of names with a Zacks Rank #1 (Strong Buy) or Zacks Rank #2 (Buy). You can’t put them all in your portfolio.

That’s where the Zacks Style Scores come in. These indicators help to narrow down that long list of stocks to increase your odds of success. They’re split into Value, Growth and Momentum scores, depending on what kind of investor you are.

But if you want everything in one place, then there’s the VGM, which combines all three styles into one score.

That’s the focus of the

Top VGM Buys screen

.

In addition to the Zacks Rank and VGM, the screen also looks for stocks in the top 50% of the Zacks Industry Rank as well as several other criteria.

Below are three names that have been on the list in recent weeks, but make sure to view the entire screen as positions are added and subtracted on a daily basis.

Micron Technology

MU

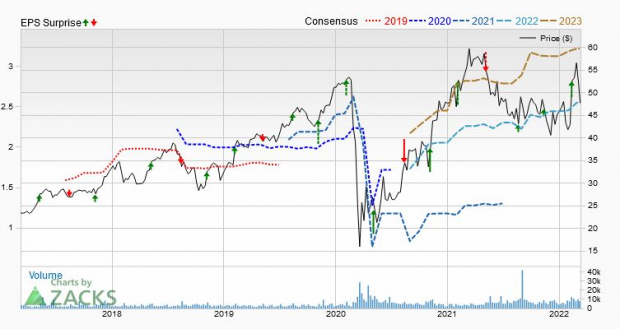

It’s hard to forget a company like Micron Technology (MU). Not only is it one of the world’s leading providers of semiconductor memory solutions, but it does business in all those innovative spaces that are building the future right now in front of our eyes. We’re talking about trends in 5G, AI (artificial intelligence) and EV (electric vehicles) adoption, which explains why the semiconductor – memory space is in the top 3% of the Zacks Industry Rank.

Micron makes high-performance memory and storage technologies, including both DRAM chips for PCs and servers, as well as NAND flash memory for smartphone and solid-state hard drives. Its segments include the Compute and Networking Business Unit (CNBU, 45% of total revenues in fiscal 2021), the Mobile Business Unit (MBU, 26%), the Storage Business (SBU, 14%) and Embedded Business Unit (EBU, 15%).

The company put together eight straight quarters of positive earnings surprises. Most recently, it reported $2.16 per share for the fiscal first quarter, which was approximately 2.9% better than the Zacks Consensus Estimate. Meanwhile, revenue of $7.69 billion jumped 33% year over year and narrowly topped our estimate.

Along with a presence in some of the growthiest avenues on the market, MU is also benefiting from a rising mix of high-value solutions, enhanced customer engagement and improvement in its cost structure.

The Zacks Consensus Estimate for this fiscal year (ending August 2022) is now $8.95, while next year’s (ending August 2023) is at $11.02. Those estimates have improved 1.1% and 5.3%, respectively, over the past three months.

Most impressively though, analysts expect year-over-year profit growth of 23%, which might end up being conservative given all the powerful secular trends in which MU is involved.

The next quarterly report is on March 29 when the company will be going for a ninth straight positive earnings surprise.

Image Source: Zacks Investment Research

Schlumberger

SLB

Oil-related companies provide one of the few sweet spots in the market right now, as the prices soars due to a one-two punch from the covid recovery and the Russia-Ukraine military conflict. So you might as well consider the largest oilfield services player on the planet… and that’s Schlumberger (SLB).

More specifically, the company helps upstream energy players locate oil and gas, and to drill and evaluate hydrocarbon wells. It also supports explorers in constructing oil and gas wells while optimizing volumes from existing ones. As part of the oil & gas – field services space, it’s in the top 41% of the Zacks Industry Rank. Shares are up approximately 46% over the past year.

SLB hasn’t missed the Zacks Consensus Estimate in several years, though it has matched a few times. The company attributed solid fourth quarter and full year performances to strengthening activity, accelerated digital sales and “outstanding” free cash flow.

In late January, SLB reported fourth-quarter earnings per share of 41 cents, which was more than 5% better than the Zacks Consensus Estimate. Revenues of approximately $6.2 billion also beat our expectations by more than 2% and improved 12.5% year over year. The company enjoyed higher contributions from Europe/CIS/Africa, a continuation of solid rig activity here in North America and increased well construction in the lucrative Gulf of Mexico.

Looking forward, SLB projects capital investment of between $1.9 billion and $2 billion in 2022, while the figure was at $1.7 billion the previous year. The company is taking advantage of the rise in fuel demand and prices, which it believes should last for the next few years.

The Zacks Consensus Estimates for this year and next are at $1.99 and $2.67, marking gains of 4.7% and 5.5%, respectively, over the past two months. However, the most impressive aspect of the raised revisions is that analysts currently expect year-over-year growth of 34.2%.

Image Source: Zacks Investment Research

Performance Food Group Company

PFGC

A major acquisition completed in September of last year has made Performance Food Group Company (PFGC) much more appetizing for investors and analysts. The Zacks Consensus Estimate is expecting year over year profit growth in the double digits for next year as expectations have been moving higher over the past several months.

PFGC markets and delivers quality food and related products to more than 300 locations, including chain restaurants, big box retailers, convenience stores and much more. As part of the food – natural foods products space, it’s in the Top 35% of the Zacks Industry Rank.

The big acquisition mentioned before was Core-Mark, which PFGC bought for $2.5 billion last year. The addition is one of the major wholesale distributors to the convenience retail industry with approximately $17 billion in net sales. It operates 32 distribution centers and serves more than 40K customer locations.

Needless to say, this acquisition enhances PFGC’s footprint in convenience and foodservice areas, which was on full display in its fiscal second quarter report.

PFGC reported earnings per share of 57 cents, which easily eclipsed the Zacks Consensus Estimate by more than 21%. Revenue of $12.84 billion soared 87.6% year over year with the Core-Mark acquisition contributing $4.2 billion of those sales.

The company expects sales between $50 billion and $51 billion for 2022, which is up from early expectations of $49.5 billion to $50.5 billion. That outlook was reaffirmed late last month.

Over the past couple of months, the Zacks Consensus Estimates have been on the rise. We now expect earnings per share of $2.55 for the year ending June 2022 and $3.22 for the year ending June 2023, which have advanced 4.5% and 3.2%, respectively. Therefore, analyst are expecting a nice 26.3% jump in profits on a year-over-year basis.

Image Source: Zacks Investment Research

Just Released: Zacks’ 7 Best Stocks for Today

Experts extracted 7 stocks from the list of 220 Zacks Rank #1 Strong Buys that has beaten the market more than 2X over with a stunning average gain of +25.4% per year.

These 7 were selected because of their superior potential for immediate breakout.

See these time-sensitive tickers now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report