Zoom Video

ZM

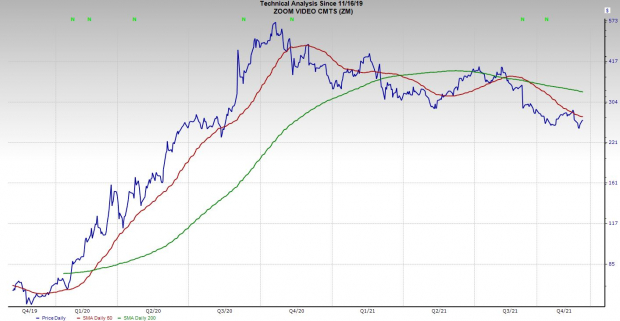

stock has tumbled over 50% from its 2020 records, including a 20% drop since its Q2 release in late August. Wall Street has dumped ZM on slowing growth, and it didn’t help that the video communication firm’s planned acquisition of Five9 Inc

(

FIVN

) fell apart.

Nonetheless, it was always going to be impossible for Zoom to match its pandemic-fueled success. Luckily, it’s still poised to grow within a vital non-email work communication space. The question now becomes is it finally time to buy Zoom stock again with its third quarter fiscal 2022 financial results due out on Monday, November 22.

Still Rather Essential

ZM’s revenue surged 88% during its first-year public after its April 2019 debut. Zoom’s software then took off during the pandemic, as businesses and countless others raced to its video communication solutions. The company’s sales skyrocketed 326% last year to $2.7 billion, driven by thousands of new paying clients.

Zoom remains essential to many businesses and other entities even as friends and family video chats have slowed down. Despite the slow return to offices—hampered by the delta variant—hybrid environments where people come in two to three days a week could possibly become the new normal for countless companies.

Many people in professional services jobs and other high-paying fields, with more leverage and the ability to change jobs more easily, found remote work life beneficial. Plus, Zoom enables businesses to cut back on travel, which was a pitch it made long before it went public. And the coronavirus might have changed the corporate travel environment for good, with the help of Zoom and others.

Zoom has expanded its portfolio from a video conferencing app to a more complete communication platform that includes Zoom Rooms, Phones, Events, and more. Cloud-based phone solutions are quickly becoming popular as businesses look for modern telecom solutions.

The goal is to have a unified place for calls, video, meetings, chat, and more. Zoom closed Q2 with 505K customers with more than 10 employees, and companies contributing over $100K in TTM revenue surged 131% to 2,278.

Image Source: Zacks Investment Research

Other Fundamentals

Investors should note Zoom and call-center software provider Five9 walked away from their planned all-stock deal in September. The deal, which was voted down by shareholders for various reasons, would have expanded its portfolio and allowed Zoom to package more offerings.

But the firm still has a strong balance sheet ($6.5 billion assets vs. $1.8 billion liabilities) and it’s spending to boost its own in-house capabilities and it will likely continue to pursue other acquisition possibilities. And Zacks estimates still call for ZM’s FY22 revenue to climb 52% to $4 billion and then pop 18% in FY23 to $4.7 billion.

Meanwhile, Zoom’s adjusted FY22 EPS are projected to climb 44% higher to $4.80 a share. This would come on top of FY21’s massive 850% growth. ZM’s FY22 and FY23 EPS estimates have popped since its report and it’s crushed our EPS estimates by an average of 35% in the last four quarters.

As we touched on up top, Zoom shares have tumbled around 50% from their highs and are down 23% since its August 30 earnings release. Despite the pullback, ZM is still up 275% in the past two years to blow away the Zacks Tech stock’s 85% climb.

Bottom Line

The stock began to pop above oversold RSI levels (30 or under) late last week and it still sits below neutral. ZM’s move higher over the last several sessions kick started its attempted return to its 50-day moving average. The much-needed pullback has also recalibrated its valuation, with it trading at over a 60% discount to its year-long high at 17.1X forward 12-month sales.

On top of that, ZM’s current Zacks consensus price target of $373 a share marks 40% upside compared to Tuesday’s levels. ZM lands a Zacks Rank #3 (Hold) right now and 10 of the 20 brokerage recommendations we have are “Strong Buys” or “Buys,” with nothing below a “Hold.”

Zacks’ Top Picks to Cash in on Artificial Intelligence

In 2021, this world-changing technology is projected to generate $327.5 billion in revenue. Now Shark Tank star and billionaire investor Mark Cuban says AI will create “the world’s first trillionaires.” Zacks’ urgent special report reveals 3 AI picks investors need to know about today.

See 3 Artificial Intelligence Stocks With Extreme Upside Potential>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report