Chemed Corporation

CHE

is gaining from robust demand for plumbing, drain cleaning and water restoration services within the Roto-Rooter arm. The company ended the first quarter of 2022 with better-than-expected earnings. A good solvency position appears promising. However, pandemic-related challenges and stiff competition do not bode well.

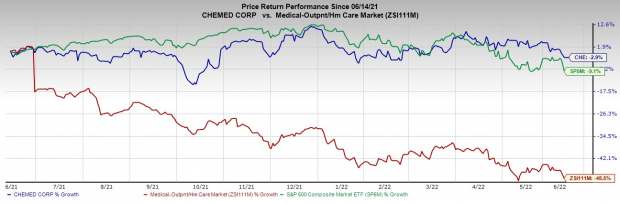

In the past year, the Zacks Rank #3 (Hold) stock has declined 2.9% against a 48.5% fall of the

industry

and a 9.1% drop of the S&P 500.

The renowned hospice care provider has a market capitalization of $6.95 billion. Chemed’s first-quarter earnings surpassed the Zacks Consensus Estimate by 6.7%.

The company projects 8.3% growth for the next five years compared with the industry and the S&P 500’s projected growth rate of 14.3% and 10.8%, respectively.

Image Source: Zacks Investment Research

Let’s delve deeper.

Factors at Play

Q1 Upsides:

Chemed’s first-quarter earnings topped the Zacks Consensus Estimate. The company registered year-over-year growth in revenues and adjusted earnings per share, instilling optimism. Robust performance by the Roto-Rooter segment drove the top line. Expansion of gross and operating margins are other advantages.

Chemed’s total home-based admissions in the first quarter rose 2.8%. Nursing home admits increased 7.8% on a year-over-year basis. The company’s average length of stay in the reported quarter was 104.8 days, up from 94.4 days in the first quarter of 2021.

Roto-Rooter Continues to Expand:

Roto-Rooter is currently the nation’s leading provider of plumbing, drain cleaning service and water restoration, providing services to over 90% of the U.S. population. In the first quarter, the segment’s revenues surged 9.4% year over year. Total branch commercial revenues rose 14.4% on a year-over-year basis, whereas total Roto-Rooter branch residential revenues registered growth of 7.2% compared with the year-ago period’s levels.

Management believes Roto-Rooter is well-positioned for growth post-pandemic and anticipates continued expansion of the segment’s market share, banking on the company’s core competitive advantages in terms of brand awareness, customer response time and 24/7 call centers and Internet presence.

Strong Solvency:

Chemed exited the first quarter of 2022 with cash and cash equivalents of $18.2 million. Meanwhile, long-term debt at first-quarter 2022-end was $120 million, higher than the current cash and cash equivalents level. Yet, while exiting the first quarter, the company did not report any short-term payable debt on its balance sheet, implying that the solvency level of Chemed is pretty promising.

Downsides

VITAS Performance Discouraging:

The VITAS segment’s revenues declined 5.3% year over year during the first quarter. The segment continued to be challenged by pandemic-related issues, including health care labor shortages, disruption in senior housing occupancy and related hospice referrals. Further, VITAS’ total admissions fell 8.9% on a year-over-year basis.

Pandemic Causes Revenue Erosion:

During the first quarter, Chemed’s average daily census was 17,313 patients, a decline of 4.1% year over year. Per management, this decline directly resulted from pandemic-related disruptions across the entire health care system since March 2020. The ongoing pandemic has also resulted in significant staffing-related challenges within the VITAS and Roto-Rooter segments.

Tough Competitive Landscape:

The market for sewer, drain and pipe cleaning and plumbing repair businesses is highly competitive. Competition is fragmented in most markets, with local and regional firms providing much of the competition. In addition, with the hospice care industry being highly fragmented, VITAS faces significant competition from many organizations based on its ability to deliver quality, responsive services.

Estimate Trend

Chemed has been witnessing a positive estimate revision trend for 2022. Over the past 90 days, the Zacks Consensus Estimate for the company’s 2022 earnings has moved 0.9% north to $19.46.

The Zacks Consensus Estimate for the company’s 2022 revenues is pegged at $2.17 billion, suggesting a 1.3% rise from the year-ago reported number.

Key Picks

A few better-ranked stocks in the broader medical space are

Alkermes plc

ALKS

,

AMN Healthcare Services, Inc.

AMN

and

Medpace Holdings, Inc.

MEDP

.

Alkermes has an estimated long-term growth rate of 25.1%. Alkermes’ earnings surpassed estimates in the trailing four quarters, the average surprise being 350.5%. It currently carries a Zacks Rank #1 (Strong Buy). You can see

the complete list of today’s Zacks #1 Rank stocks here.

Alkermes has outperformed the industry over the past year. ALKS has gained 11.1% compared with the industry’s 44.7% decline in the said period.

AMN Healthcare has a long-term earnings growth rate of 1.1%. The company surpassed earnings estimates in the trailing four quarters, delivering a surprise of 15.6%, on average. It currently flaunts a Zacks Rank #2 (Buy).

AMN Healthcare has outperformed its industry in the past year. AMN has gained 5.1% against the industry’s 66.5% fall.

Medpace has a historical growth rate of 27.3%. Medpace’s earnings surpassed estimates in the trailing four quarters, the average surprise being 17.1%. It currently has a Zacks Rank #2.

Medpace has outperformed its industry in the past year. MEDP has declined 22.5% compared with the industry’s 66.5% fall.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +25.4% per year. So be sure to give these hand-picked 7 your immediate attention.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report