Ulta Beauty, Inc.

ULTA

appears to be a lucrative pick with solid growth prospects. The company has been gaining from its strong omnichannel business and skincare category advancement. Also, a focus on six key priorities has been working well for this beauty retailer, which raised its fiscal 2022 guidance on its first-quarter earnings release.

On its last earnings call, management stated that due to a solid first-quarter show and sales trends witnessed in the second quarter so far, it raised its guidance for fiscal 2022. It now expects fiscal 2022 net sales in the range of $9.35-$9.55 billion compared with the $9.05-$9.15 billion range expected earlier. Comparable sales or comps are expected to rise in the range of 6-8% now compared with the earlier view of 3-4%. Comps are likely to be in the low-to-mid-teens range in the first half and moderate to a low-single-digit rise in the second half.

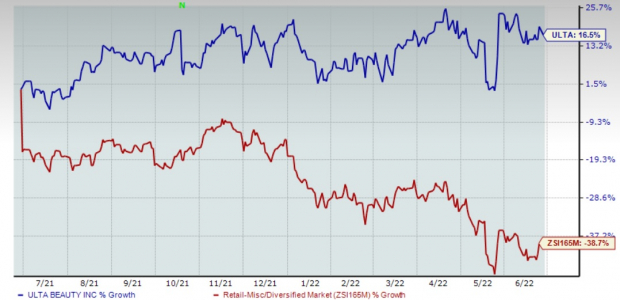

Management now expects the operating margin between 14.1% and 14.4%, which was earlier expected between 13.7% and 14%. For fiscal 2022, earnings are envisioned in the range of $19.20-$20.10 per share now, up from the $18.2-$18.7 per share range expected before. Shares of this Zacks Rank #1 (Strong Buy) company have rallied 16.5% in the past year against the

industry

’s decline of 38.7%. Let’s delve deeper into the factors backing this Illinois-based player.

Image Source: Zacks Investment Research

Omnichannel Strength

Ulta Beauty has been enriching its omnichannel experience through launches like Beauty to Go, options like same-day delivery (in some stores) and unique salon services across stores, among others. In the first quarter of fiscal 2022, the company opened 26 Ulta Beauty at Target shops and ended the quarter with 127 locations. Apart from this, ULTA is benefiting from its Wellness Shop launch (in the fourth quarter of fiscal 2021), which is a cross-category platform providing guests with self-care for the mind, body and spirit across several stores and online. On its first-quarter earnings call, management stated that its Wellness Shop reached nearly 55% of its store fleet. The company’s buy online, pick up in store (BOPIS) continued to gain traction in the first quarter. BOPIS sales rose 26% and contributed 21% to e-commerce sales.

Skincare Category – a Major Driver

Ulta Beauty has been seeing market share gains in major beauty categories for a while now, with skincare standing out due to consumers’ rising interest in self-care and the company’s focus on newness and innovation. The trend continued in the first quarter of fiscal 2022, wherein skincare comps saw strong double-digit growth. Category growth was backed by moisturizers, acne treatments and eye serums. Guests’ increased focus on self-care and maintaining healthy skincare routines works well for this category. Apart from these, the company has been seeing strength in the fragrance and haircare category, with product newness being a solid driver. Even the makeup category is on track for full recovery.

Ulta Beauty Inc. Price, Consensus and EPS Surprise

Ulta Beauty Inc. price-consensus-eps-surprise-chart

|

Ulta Beauty Inc. Quote

Focus on Key Priorities

The company’s foremost priority is to strengthen its omnichannel business and explore the potential of both physical and digital facets. Ulta Beauty has made significant progress on this front, evident from its solid e-commerce initiatives. Next, the company is undertaking various tools to enhance the experience of guests, like offering a virtual try-on tool and in-store education and reimagining fixtures, among others. Thirdly, the company concentrates on offering customers a curated and exclusive range of beauty products through innovation. Fourthly, ULTA is focused on deepening customer engagement by boosting rewards and loyalty programs. Fifthly, management is committed to optimizing its cost structure. Apart from these, the company strives to boost organizational talent and strengthen the culture.

Hence, Ulta Beauty looks well-positioned for growth. The current Zacks Consensus Estimate for fiscal 2022 earnings per share (EPS) has risen by a penny to $20.08 over the past seven days.

Other Solid Picks You May Look at

Here are some other similar-ranked stocks –

Kroger Co.

KR

,

Dillard’s, Inc.

DDS

and

Dollar Tree

DLTR

.

Dillard’s, which operates retail department stores, sports a Zacks Rank #1. The company has a trailing four-quarter earnings surprise of 224.1%, on average. You can see

the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Dillard’s current financial-year sales suggests growth of 6.1% from the year-ago period. DDS has an expected EPS growth rate of 14.6% for three to five years.

Kroger, a renowned grocery retailer, sports a Zacks Rank #1. Kroger has a trailing four-quarter earnings surprise of 20.3%, on average.

The Zacks Consensus Estimate for KR’s current financial-year sales and EPS suggests growth of 6.7% and 5.7%, respectively, from the year-ago period.

Dollar Tree, a discount variety retail store operator, sports a Zacks Rank #1. The company has an expected EPS growth rate of 15.5% for three to five years.

The Zacks Consensus Estimate for Dollar Tree’s current financial-year sales suggests growth of 6.7% from the year-ago period. DLTR has a trailing four-quarter earnings surprise of 13.1%, on average.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2021. Previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report