Semiconductors, also called microchips, are a highlight of technology – they exist in almost every aspect of our lives. From freezers to computers, they allow the devices we rely on daily to work smoothly and efficiently.

Two titans in the semiconductor arena – Advanced Micro Devices

AMD

and Nvidia

NVDA

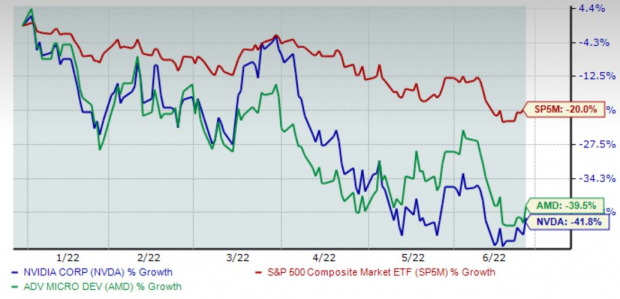

– have quickly become two of the go-to stocks when investing in this lucrative space. 2022 has not been kind to either of these companies, as illustrated in the year-to-date chart below that compares the two while blending in the S&P 500 for a benchmark.

Image Source: Zacks Investment Research

A hawkish Fed, supply-chain issues, and a widespread microchip shortage have played spoilsport for most semiconductor-related and technology companies. These once high-flying stocks that displayed zero signs of ever slowing down have almost come to a complete halt in 2022.

Below is a five-year chart of both companies while blending in the S&P 500 for a benchmark.

Image Source: Zacks Investment Research

As we can see, both companies have had meteoric rises, easily outpacing and crushing the S&P 500. Investors in these stocks have undoubtedly reaped considerable gains.

Now that both companies’ shares have pulled back extensively, it raises a valid question – which company is currently a better investment? Let’s take a look at forecasted growth, recent earnings performance, and valuation levels to get a better view of the matter.

Advanced Micro Devices

Advanced Micro Devices

AMD

is a multinational semiconductor company that develops computer processors and related technologies for business and consumer markets.

Its rough stretch throughout 2022 has caused its forward earnings multiple to retrace down to 20.5X, which is nowhere near 2020 highs of 107.2X and well below highs earlier this year of 63.1X. The value represents a 21% premium relative to the S&P 500’s forward earnings multiple of 16.9X.

AMD has a Style Score of a C for Value.

The company has consistently posted strong bottom-line results, exceeding EPS estimates in eight consecutive quarters dating back to June 2020. In its latest quarterly report, the company exceeded EPS expectations by a notable double-digit 24% and has beat EPS estimates by an average of 18% over its last four quarters.

Additionally, the company has exceeded revenue estimates in ten consecutive quarters, undoubtedly a major positive that shows the company’s health.

For the upcoming quarter, analysts have been pushing their EPS estimates higher, reflecting quarterly earnings of $1.03 per share and displaying a substantial 64% growth in the bottom-line from the year-ago quarter. For the full fiscal year, the $4.37 EPS estimate represents a sizable 56% growth in the bottom-line year-over-year.

In fact, analysts have been upping their earnings outlook across the board.

Image Source: Zacks Investment Research

Nvidia

Nvidia

NVDA

is the worldwide leader in visual computing technologies and is recognized as the inventor of the highly successful graphic processing unit (GPU).

The company’s forward earnings multiple has fallen to 35.7X, undoubtedly a pricey point. However, the value is a fraction of its 93.5X high in 2021 and well below its five-year median of 49.8X. Additionally, shares trade at a rich triple-digit 110% premium relative to the S&P 500.

NVDA has a Value Style Score of a D.

Image Source: Zacks Investment Research

NVDA has become known for strong quarterly reports, exceeding bottom-line expectations in a jaw-dropping 14 consecutive quarters dating back to early 2019. In its latest quarter, the company exceeded EPS expectations by nearly 5%; over its last four quarters, it has beat EPS estimates by an average of 5.3%.

Furthermore, the company has beaten quarterly revenue estimates in 13 consecutive quarters.

Analysts have been dialing back their earnings estimates across all timeframes over the last 60 days. For the upcoming quarterly release, the Consensus Estimate Trend has fallen 4.5%, reflecting EPS of $1.27 and a notable 22% increase in the bottom-line from the year-ago quarter. Additionally, the current fiscal year EPS estimate of $5.47 reflects a strong 23% increase in earnings year-over-year.

Image Source: Zacks Investment Research

Bottom Line

It isn’t easy to choose between these two powerhouses. Both have generated immense gains over the last several years and have undoubtedly been a staple in many portfolios.

Now that the music has seemingly been shut off in 2022, the fun has halted. It’s not for just these two companies, however, the entirety of tech and high-growth stocks have undergone deep valuation slashes throughout 2022.

A hawkish Fed, supply chain issues, and of course, a chip shortage have all been impactful driving forces behind the sell-offs.

As of now, I currently believe that AMD would be a wiser investment, and here’s why – AMD shares have been stronger year-to-date, the company has more enticing valuation levels, and analysts have been upping their earnings outlook across the board over the last 60 days.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +25.4% per year. So be sure to give these hand-picked 7 your immediate attention.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report