Veeva Systems Inc.

VEEV

has been gaining from its robust product adoption. A solid performance in the first quarter of fiscal 2022 and a slew of partnerships buoy optimism on the stock. However, foreign-exchange fluctuations and a tough competitive landscape are major downsides.

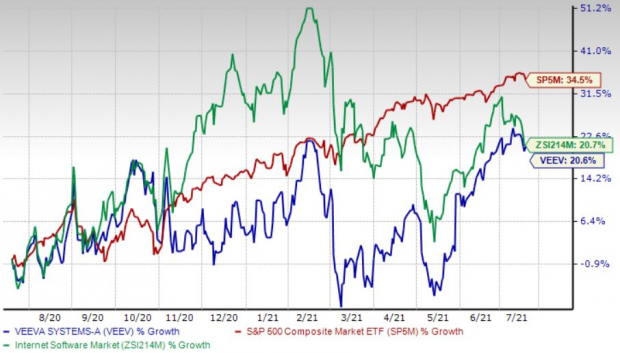

Over the past year, the Zacks Rank #2 (Buy) stock has gained 20.6% compared with 20.8% growth of the

industry

and 34.6% rise of the S&P 500.

The renowned provider of cloud-based software applications and data solutions for the life sciences industry has a market capitalization of $48.23 billion. The company projects 15.8% growth for the next five years and expects to witness continued improvements in its business. Veeva Systems surpassed the Zacks Consensus Estimates in all the trailing four quarters, the average surprise being 14.65%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Robust Product Adoption:

Veeva Systems has been registering a solid uptake for its products over the past few months. The company, in June, announced that Oval Medical Technologies Ltd and inveox GmbH are using Veeva Vault Quality Suite applications to modernize quality management and drive greater GxP compliance.

In May, Veeva Systems announced that with the growing need for greater efficiency in clinical studies, more than 100 organizations are simplifying trial management and monitoring via the sturdy adoption of Veeva Vault CTMS (clinical trial management system).

Strategic Partnerships:

Veeva Systems has forged a slew of partnerships over the past few months, raising our optimism. The company, in May, announced a strategic partnership with Oncopeptides to support the launch of the latter’s first commercial product.

In April, Veeva Systems entered into a strategic collaboration with Parexel to accelerate clinical trials through technology and process innovation. In February, the company inked a deal with Impel NeuroPharma to expedite the pre-launch preparation for Impel’s migraine treatment, INP104, which has been accepted for review by the FDA and will be marketed under the trade name TRUDHESA once approved.

Strong Q1 Results:

Veeva Systems’ better-than-expected results in first-quarter fiscal 2022 instill confidence in the stock. Both segments performed impressively during the quarter. The company continues to benefit from its flagship Vault platform, which is encouraging. Strength in core CRM and the expanding market share, along with customer wins, look impressive. A slew of product launches over the past few months looks encouraging as well. Expansion of both margins bodes well. A raised guidance for the fiscal year is another major positive.

Veeva Systems’ exposure to currency movement as it rakes in a significant portion of its sales from international markets remains a headwind. With expanding operations in countries outside the United States, a chunk of its revenues and expenditures in future may be denominated in foreign currencies. Fluctuations in the value of U.S. dollar versus foreign currencies may impact its operating results when translated into U.S. dollars.

Veeva Systems operates in a highly competitive market. In new sales cycles within the company’s largest product categories, it competes with other cloud-based solutions from providers that develop applications for the life sciences industry. The company’s Commercial Cloud and Veeva Vault application suites also vie to replace client server-based legacy solutions offered by its rivals.

Estimate Trend

Veeva Systems has been witnessing an upward estimate revision trend for 2022. Over the past 90 days, the Zacks Consensus Estimate for its earnings per share has moved 8.7% north to $3.50.

The Zacks Consensus Estimate for second-quarter fiscal 2022 revenues is pegged at $451.2 million, suggesting a 27.6% rise from the year-ago reported number.

Other Key Picks

A few other top-ranked stocks from the broader medical space are

Henry Schein, Inc.

HSIC

,

AMN Healthcare Services Inc

AMN

and

Align Technology, Inc.

ALGN

.

Henry Schein’s long-term earnings growth rate is estimated at 11.2%. The company presently carries a Zacks Rank #2. You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

AMN Healthcare’s long-term earnings growth rate is estimated at 6.5%. It currently carries a Zacks Rank #2.

Align Technology’s long-term earnings growth rate is estimated at 23.2%. It currently carries a Zacks Rank #2.

5 Stocks Set to Double

Each was hand-picked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2021. Each comes from a different sector and has unique qualities and catalysts that could fuel exceptional growth. Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report