Paycom Software

PAYC

is one of the stocks investors should currently add to their portfolio to shrug off highly volatile market conditions and benefit from its upside potential.

From the start of 2022, Wall Street has been witnessing high volatility due to several ongoing economic tensions, such as the outbreak of new COVID-19 variants, skyrocketing crude oil prices, rising inflationary pressure and a shift in Fed’s policy to a tougher-than-expected line. Moreover, the ongoing Russia-Ukraine conflict remains a key concern among potential investors.

Such geopolitical uncertainties are likely to continue to weigh on investors’ sentiments, which might eventually bring higher volatility to the U.S. equity market. Year to date (“YTD”), the Dow Jones Industrial Average, Nasdaq Composite and S&P 500 have plunged 16%, 30.9% and 21.3%, respectively.

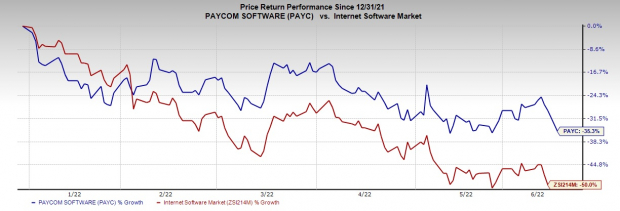

In such a scenario, top-ranked stocks like Paycom can boost one’s portfolio. PAYC’s price trend reflects that the stock has an impressive run on the bourse YTD. Shares of the company have decreased 35.3% compared with the Zacks

Internet-Software

industry, which slumped 50% YTD.

Image Source: Zacks Investment Research

Why Is PAYC an Attractive Pick?

Trading Way Below 52-Week High

: Paycom stock currently trades lower than its 52-week high, which reflects its potential to go upward. The stock’s closing price of $268.50 on Jun 13 is 52% lower than the 52-week high of $558.97 attained on Nov 2, 2021.

Attractive Valuation

: Paycom currently trades at an attractive valuation multiple. The stock trades at a one-year forward price-to-sales multiple of 10.97X compared with its five-year average of 14.99X.

Solid Rank & Growth Score

: Paycom currently sports a Zacks Rank #1 (Strong Buy) and has a

Growth Score

of B. Our research shows that stocks with a Growth Score of A or B, when combined with a Zacks Rank #1 or #2 (Buy), offer the best investment opportunities to investors. Thus, the company appears to be a compelling investment proposition at the moment.

Positive Earnings Surprise History

: PAYC has an impressive earnings surprise history. The company outpaced estimates in the trailing four quarters, delivering an average earnings surprise of 7.2%.

Strong Earnings Growth Potential

: The Zacks Consensus Estimate of $5.53 per share for 2022 earnings suggests year-over-year growth of approximately 23.4%. The consensus mark for 2023 earnings indicates a 25.1% year-over-year surge and is pegged at $6.92 per share. Moreover, the long-term expected earnings growth rate for the stock is pegged at 25%.

Robust Fundamental Growth Drivers

: Paycom is benefiting from the increased top line as a result of new client additions and a continuous focus on cross-selling to its existing clients.

The company’s differentiated employee strategy, measurement capabilities and comprehensive product offerings are helping it win new customers.

Per the latest

Skyquest

report, the global software-as-a-service (SaaS) market is expected to reach $720.44 billion by 2028, witnessing a CAGR of 25.89% during the 2022-2028 forecast period. With its SaaS-based applications, Paycom is well-positioned to lead the market.

Paycom’s constant efforts for client retention aided it in increasing its average annual client retention rate from 91% in 2017 to 94% in 2021. It has a huge client base and is gaining foothold among larger companies. The company is expanding its proactive sales efforts to target companies with 50 to 10,000 employees compared with its prior target of 50 to 5,000 employees. Considering its growth prospects, it makes sense to invest for long-term gains.

Other Stocks to Consider

Some other top-ranked stocks from the broader

Computer and Technology

sector are

Axcelis Technologies

ACLS

,

Baidu

BIDU

and

Analog Devices

ADI

. While Axcelis and Baidu each sport a Zacks Rank #1, Analog Devices carries a Zacks Rank of 2. You can see

the complete list of today’s Zacks #1 Rank stocks here

.

The Zacks Consensus Estimate for Axcelis’ second-quarter fiscal 2022 earnings has been revised 3 cents northward to 99 cents per share over the past 60 days. For 2022, earnings estimates have moved 10.3% north to $4.40 per share in the past 60 days.

Axcelis’ earnings beat the Zacks Consensus Estimate in each of the preceding four quarters, the average surprise being 23.5%. Shares of ACLS have soared 30% in the past year.

The Zacks Consensus Estimate for Baidu’s second-quarter 2022 earnings has been revised 31 cents southward to $1.38 per share over the past 30 days. For 2022, earnings estimates have moved 3 cents north to $8.27 per share in the past 30 days.

Baidu’s earnings beat the Zacks Consensus Estimate in each of the preceding four quarters, the average surprise being 52.9%. Shares of BIDU have dipped 29.3% in the past year.

The Zacks Consensus Estimate for Analog Devices’ third-quarter fiscal 2022 earnings has been revised upward by 5 cents to $2.42 per share over the past 30 days. For fiscal 2022, earnings estimates have moved 16 cents north to $9.24 per share in the past 30 days.

Analog Devices’ earnings beat the Zacks Consensus Estimate in each of the preceding four quarters, the average surprise being 7.7%. Shares of ADI have decreased 11.9% in the past year.

How to Profit from the Hot Electric Vehicle Industry

Global electric car sales in 2021 more than doubled their 2020 numbers. And today, the electric vehicle (EV) technology and very nature of the business is changing quickly. The next push for future technologies is happening now and investors who get in early could see exceptional profits.

See Zacks’ Top Stocks to Profit from the EV Revolution >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report