When a publicly traded company announces layoffs, it can often boost to the underlying stock price. Though this seems illogical, there are a couple of reasons this could occur.

First, layoffs can indicate that the company is trying to cut costs to improve its financial health in a tough economy. Second, job cuts can signal that the management team is focused on agility, financial efficiency, and increasing the bottom line.

Lastly, it is essential to consider that layoffs can have various impacts on a stock depending on the situation. For instance, if the layoffs are seen as desperate and a product of financial troubles, it will often impact shares negatively. Conversely, if the cuts are viewed as a long-term strategy to cut costs in an otherwise strong company, the stock will often react positively.

Early Wednesday, shares of software giant

Salesforce

CRM

rose after management announced that the company would be cutting 10% of its workforce. Salesforce, the worldwide leader in Customer Relationship Management (CRM) software, was an unusual beneficiary of the pandemic. As more and more employees moved to work from home, demand for its product grew years ahead of schedule, and the stock outperformed.

Image Source: Zacks Investment Research

Pictured: CRM outperformed dranatically during the pandemic but fell recently with most of tech.

However, recently, the stock has come back to Earth and underperformed as a bloated valuation, tech wreck, and the pandemic euphoria finally wearing off took its toll. So where does CRM stand now?

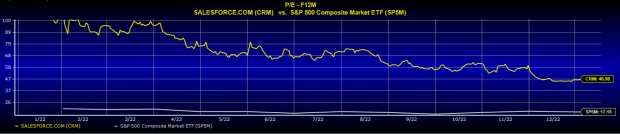

Image Source: Zacks Investment Research

Pictured: CRM’s P/E is shrinking as shares fall.

From a valuation perspective, the stock is getting more attractive, although shares are still expensive relative to the S&P 500 Index. For the trailing twelve-month period, CRM’s P/E of 30.56X is still bloated compared to the Zack’s Computer – Software industry’s P/E of 24.56X. Earnings growth slowed to just +10% last quarter, though it improved over the previous two quarters. One thing the bull camp can point to is the company’s consistency in beating earnings estimates. Salesforce has surprised on earnings for 20 straight quarters.

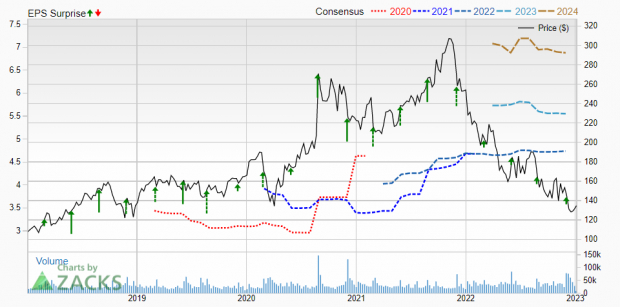

Image Source: Zacks Investment Research

Pictured: CRM has consistently surprised to the upside on earnings.

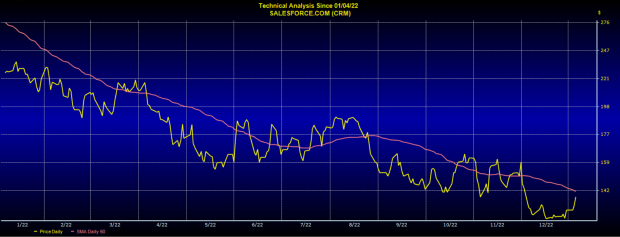

From a technical perspective, CRM is stuck in a downtrend and approaching the 50-day moving average from below – an area of resistance.

Image Source: Zacks Investment Research

Pictured: Shares are bumping up against 50-day moving average resistance.

Takeaway

It may be too early for investors to jump aboard shares of Salesforce, although the stock is getting more attractive. Investor sentiment is shifting in the short-term after the layoff announcement. Valuation is moving closer to sustainable levels, nearly matching its industry peers. With that said, technical hurdles are still in the way, and the company will need to show healthier growth when it reports earnings in its March quarter if it wants to sustain an upside move.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report